Mortgage Rates: Today's Rates, 30-Year Trends & Refinance Signals

Decoding the Daily Mortgage Rate Mirage: Beyond the Headlines

Another Thursday, another set of numbers flashing across our screens. On November 27, 2025, NerdWallet reported the average 30-year fixed-rate mortgage holding steady at 6.05% APR. The 15-year fixed nudged down two basis points (that’s 0.02% for the uninitiated, a seemingly tiny fraction that compounds into real money), landing at 5.47% APR. Even the 5-year adjustable-rate mortgage (ARM) saw a four-basis-point drop to 6.66% APR. On the surface, it’s a quiet day, a minor blip in the grand scheme. But as any seasoned analyst knows, the surface rarely tells the full story.

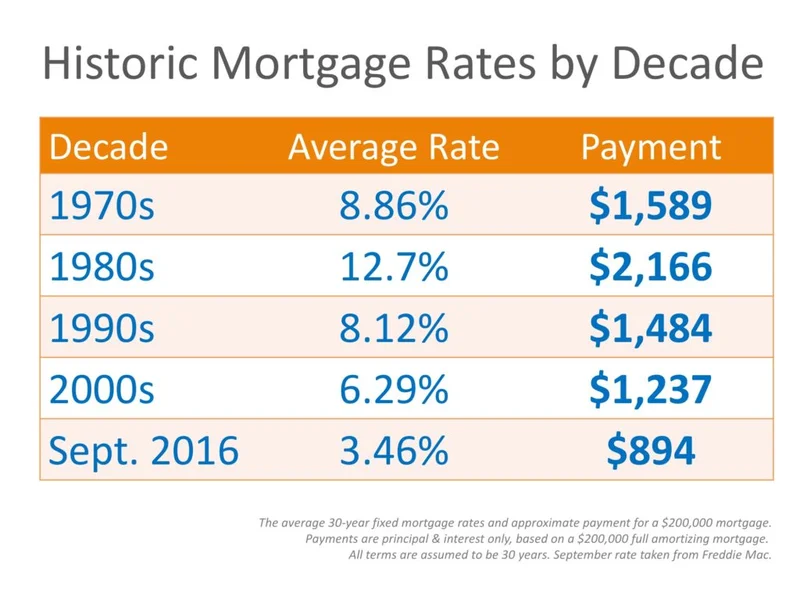

What’s truly striking, if you're sifting through these data points as I am, is the subtle, almost imperceptible shift. That 30-year fixed rate? It's seven basis points lower than just a week ago, and a more substantial 49 basis points lower than this time last year. That’s nearly half a percentage point, a move that would have felt like a seismic event just a few months back when rates seemed glued to the stratosphere. This isn't just a daily tick; it's part of a larger, downward trajectory, even if the daily movements are as subtle as a whisper in a crowded room.

The Illusion of a Single "Today's Rate"

Here’s where the analytical mind starts to itch. NerdWallet, citing Zillow data for November 27, pegs the 30-year fixed at 6.05%. Yet, a report from Money, also citing Zillow, states the average 30-year mortgage rate for November 26, 2025, was 5.99%. That’s a six-basis-point difference for what is essentially the same timeframe and source data. This isn't a minor rounding error; it's a significant variance when we're talking about the precision of basis points.

If two reputable sources, drawing from the same underlying data provider, can't quite agree on the exact figure for what "today's rate" actually is, then what exactly are borrowers supposed to anchor their expectations to? It's like trying to hit a moving target in the fog. This isn't an indictment of the data providers themselves, but rather a methodological critique of how these "average rates" are presented and consumed. They are, by definition, averages, sample rates based on generic borrower characteristics. They're a compass bearing, not a GPS coordinate, and that's a distinction far too many miss.

The "Nerdy take" from NerdWallet points to a "short week, without a lot of new economic data to steer mortgage rates in any particular direction." Yet, they immediately pivot to the market's conviction that the Federal Reserve will cut short-term rates in December. This is the financial market's equivalent of a dog hearing a can opener: the action hasn't happened yet, but the expectation alone is enough to send a ripple through the system. I've looked at hundreds of these rate reports, and the market's pre-emptive pricing of a Fed move is a fascinating, almost predictive, dance. It suggests that much of the "downward step" we've seen this week isn't a reaction to new information, but rather the market solidifying its bet on future action.

The Fed's Shadow and Your Personal Equation

This anticipatory mood from the Fed isn't just abstract chatter for bond traders; it's creating a very real, tangible opportunity. For hundreds of thousands of homeowners with rates around 7% (and let’s be honest, many bought when rates were even higher than that in early 2025), this downward trend marks a genuine refinance opportunity. The difference between 7% and, say, 6.05% or even 5.99%, isn't just pocket change. As Freddie Mac research demonstrates, comparing just two lenders can save you $600 per year—to be more exact, comparing at least four lenders can bump that annual savings to up to $1,200. Over the life of a 30-year loan, that's almost $22,000 less in interest on a $360,000 mortgage for just a quarter-point difference. It’s a substantial amount of capital that could be better deployed elsewhere. For those considering refinancing, it's worth checking out a Current refi mortgage rates report for Nov. 24, 2025 to get a sense of the current landscape.

But here’s the rub, and it’s a critical one: these advertised rates are merely the starting gun. Your actual mortgage rate is a deeply personal equation, a complex algorithm based on factors you can control and forces you absolutely cannot. Your credit score, your down payment, the type of loan you choose, even how you plan to use the home (primary residence vs. investment property)—these are all variables that lenders plug into their internal models. A high credit score and a hefty down payment are seen as de-risking factors, almost always translating to a lower rate offer.

Then there are the macro forces: the U.S. economy, global economic shifts, inflation, the job market, and of course, the Federal Reserve. These are the tides, and you're just trying to navigate your small boat. A hot housing market, for instance, can reduce the incentive for lenders to compete aggressively, potentially leading to higher rates regardless of other factors. So, while the broad trends are important, the micro-level negotiation, driven by your personal financial profile, is paramount. Given the sheer number of variables, are we truly talking about "mortgage rates" or a million individual interest rate probabilities?

Your Rate, Not the Headline's

The prevailing narrative is that rates are dropping, and the market anticipates further cuts from the Fed. This is good news, particularly for those looking to refinance or enter the market. The average 30-year fixed purchase rate sitting just under 6% (or slightly above, depending on which timestamp you trust) is a far cry from the 7%+ figures that became depressingly common.

However, a critical piece of advice often gets buried in the enthusiasm: shop around. Don't settle for the first quote. The difference between lenders can be substantial. And be wary of phrases like "float-down options" for a new, lower rate – they almost invariably come "for a fee." Always calculate if that fee truly justifies the potential savings. The headline rate is a siren song; your personalized Loan Estimate is the map. Ignore the former at your financial peril, and scrutinize the latter with the precision of a seasoned auditor. The only rate that truly matters is the one you lock in, tailored to your specific financial reality.